- Bengaluru leads in office transactions with 5.3 mn sq ft of leasing in Q3 2024

- GCCs lead market volumes in Q3 2024 with 7.1 mn sq ft

- Bengaluru rents grow by 7% YoY

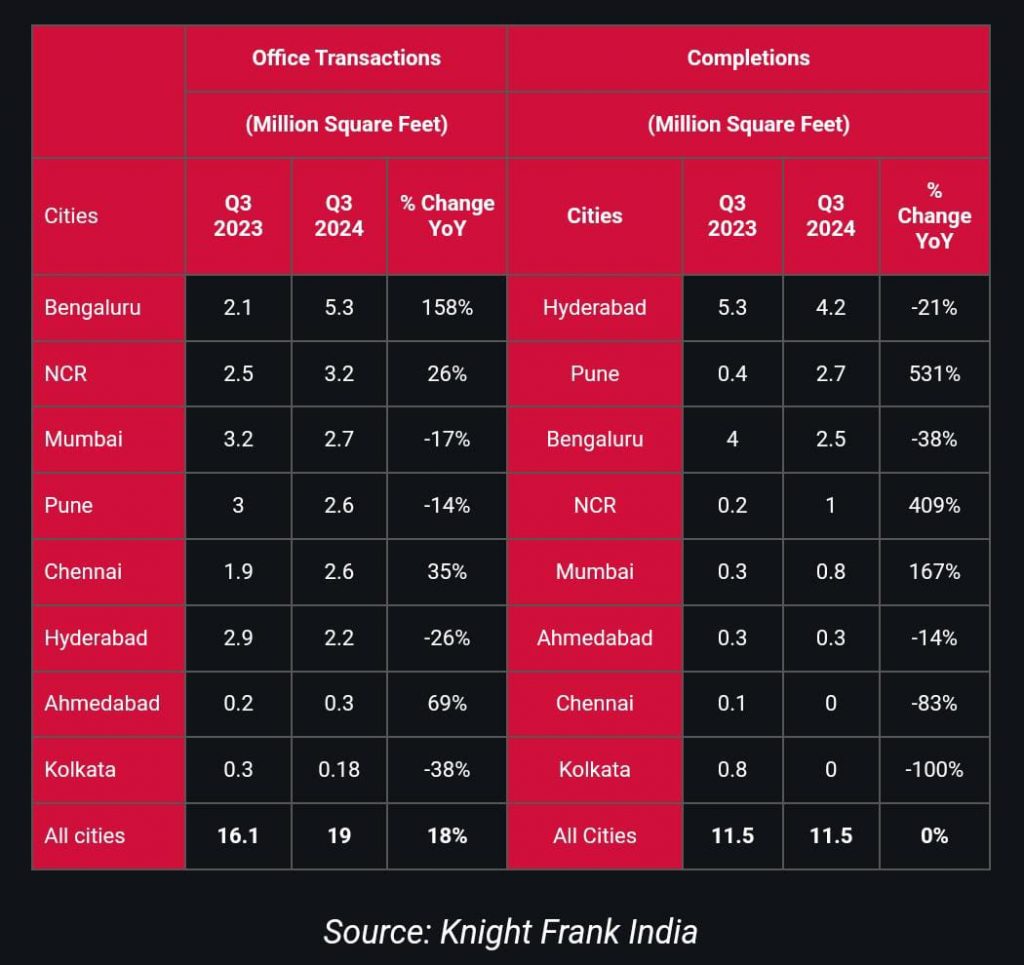

Mumbai, October 3, 2024: In its latest report on India Real Estate: Office and Residential Market for July – September 2024 (Q3 2024), Knight Frank India revealed that office space transactions reached 19 million square feet (mn sq ft), the highest quarterly absorption since Q1 2018. This marks an 18% year-on-year (YoY) increase from 16.1 mn sq ft in Q3 2023. In year-to-date terms, 2024 has already registered leasing of 53.7 mn sq ft, 27% higher YoY, in the first 9 months of the year, and is on course to breach a fresh annual high in 2024.

Global Capability Centers (GCCs) accounted for 7.1 mn sq ft or 37% of the transacted volume during Q3 2024, while India Facing businesses took up 6.6 mn sq ft or 35% of the transacted volumes.

The strong demand in office market reflects the confidence of businesses focused on the Indian economy amid ongoing growth while the increased interest from GCCs highlights global enterprises’ high commitment to the Indian business environment.

Bengaluru office market which recorded the highest volume of transactions for Q3 2024 at 5.3 mn sq ft constituted 28% of the office volume transactions across eight cities in the country. The transactions in the city grew substantially by 158% YoY and to 5.3 mn sq ft in Q3 2024. NCR and Chennai which grew at 26% and 35% YoY respectively were the other prominent markets to record significant growth.

Shishir Baijal, Chairman and Managing Director, Knight Frank India said, “India’s sustained economic growth is driven by strong business performance, and the positive sentiment is clearly reflected in the strength of the office market. India-facing businesses and GCCs have continued to expand operations, remaining the primary drivers of increased volumes. We expect this trend to continue for the rest of the year, with the possibility of office leasing numbers crossing 70 million sq ft by the end of 2024—an astounding 10 million sq ft increase, or a 20% growth over the previous high. This exceptional growth underscores India’s position as a thriving global business hub.”

All India Office Update: July – September 2024 (Q3 2024)

Experiencing a remarkable 18% YoY growth, the Indian office space market maintained its momentum into Q3 2024 following a robust performance throughout 2024. Leading the charge, Bengaluru emerged as a standout performer, witnessing a staggering 158% YoY surge in office space transactions.

Global Capability Centers accounted for 37% share in the Q3 2024, 7.1 mn sq fttaken up by GCCs counts as the largest share of the transactions’ pie. Of the total spaces transacted by GCCs in this quarter, 47% was concentrated in Bengaluru.

India facing businesses, which have traditionally anchored the market, accounted for 35% of the transacted volumes in Q3 2024. This can be attributed to the high level of confidence in the outlook for the Indian economy and steady growth of consumer markets.

Flex space operators accounted for 16% of the total transacted volume. Volumes taken up by Third Party IT services have trended up well in 2024 2.6 mn sq ft transacted in Q3 2024, constituting a 115% growth in YoY terms.

Viral Desai, Senior Executive Director, Occupier Strategy & Solutions, Industrial & Logistics, Capital Markets and Retail, Knight Frank India, said,”The office market in India has been expanding steadily, driven by strong demand from Global Capability Centres (GCCs) and India-facing businesses. As more companies bring employees back to the office, either partially or fully, demand for office space is strengthening over the last few quarters. Rental growth across key markets remains healthy, supporting by sustained volume growth. The momentum in development activity is building up as well with occupier Wellness and ESG compliance gaining increasing focus.”

Notes:

- India Facing: These refer to such transactions whose lessees/buyers are businesses which have an India focused business, i.e., no export or import.

- Third Party IT Services: These refer to transactions whose lessees/buyers are focused on providing IT and IT enabled services to offshore clients. They service multiple clients and are not necessarily owned by any of their clientele.

- Global Capability Center (GCC): These refer to transactions whose lessees/buyers are focused on providing various services to a single offshore company. The offshore company has complete ownership of the entity that has transacted the space.

- Flex Space: These refer to transactions by companies that specialise in providing comprehensive office space solutions for other businesses along with the benefits of flexibility of tenure, extent of services provided and the ability to scale higher or lower as required.

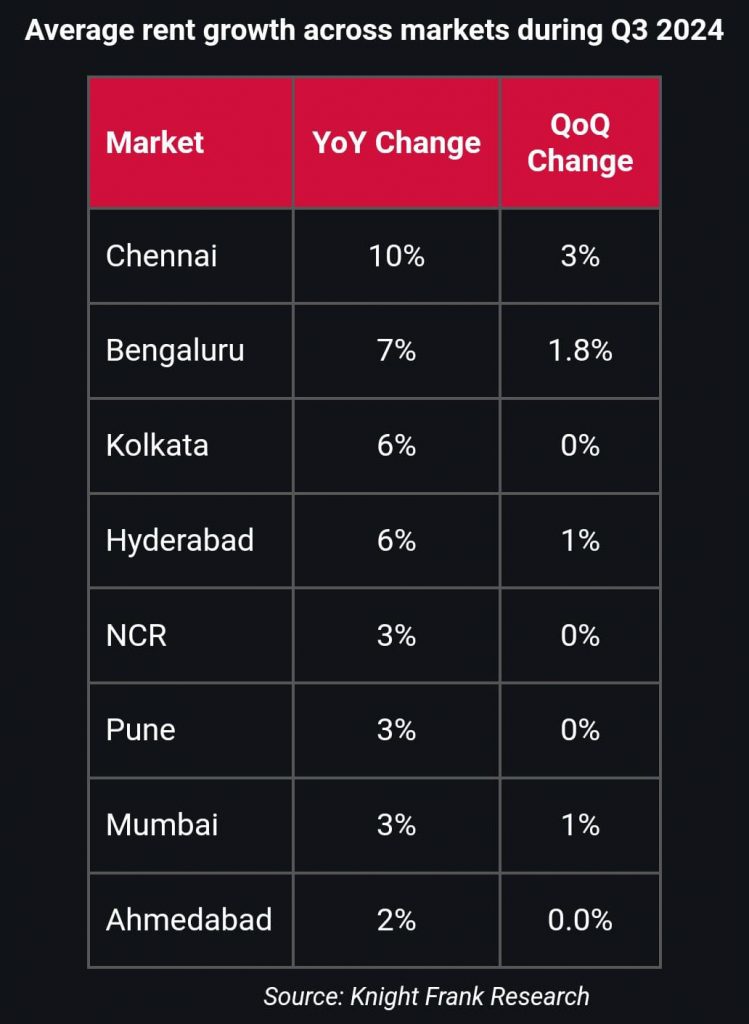

| Ninth Consecutive Quarter Exhibit Rental Stability or Growth |

In Q3 2024, rental values grew across all markets YoY. Notably, this marks the ninth consecutive quarter with either stable or positive YoY rent movement. Rents in the larger office markets of NCR, Mumbai and Pune grew by 3% YoY while Bengaluru and Chennai rents grew by 7% and 10% YoY respectively.